Making money from making money

Who has control over the supply of new money and what benefits does it bring?

31 January 2017

Who has control over the supply of new money and what benefits does it bring?There is now widespread acceptance that in modern economies, commercial banks, rather than the central bank or state, create the majority of the money supply.

This report, written by the New Economics Foundation and Copenhagen Business School, examines ‘seigniorage’ – the profits that are generated through the creation of money. We show that in the UK, commercial bank seigniorage profits amount to a hidden annual subsidy of £23 billion, representing 73% of banks’ profits after provisions and taxes.

Seigniorage has traditionally been understood as the difference between the cost of physically producing money and its purchasing power in the economy – a £10 note for example costs just a few pence to produce so seigniorage profits are likely to be close to £10. Historically it was sovereign states who had the exclusive power to create and spend money in to the economy: the term seigniorage derives from the French seignior which means sovereign ruler or feudal Lord.

In modern economies, such as the UK, however, money in circulation created by the state – physical cash – only represents around 3% of the total money supply. The remaining 97% is lent in to economies as the digital IOUs of commercial banks – the deposits that are entered in to our bank accounts when banks make new loans.

This report develops a model of commercial bank seigniorage based on the reality that banks, unlike other financial intermediaries such as Peer2Peer (P2P) lending platforms, do not have to acquire funds in the first instance before making loans. This is because banks’ IOUs – bank deposits – have been privileged by the state as having the status of money which people must hold to make payments in the economy.

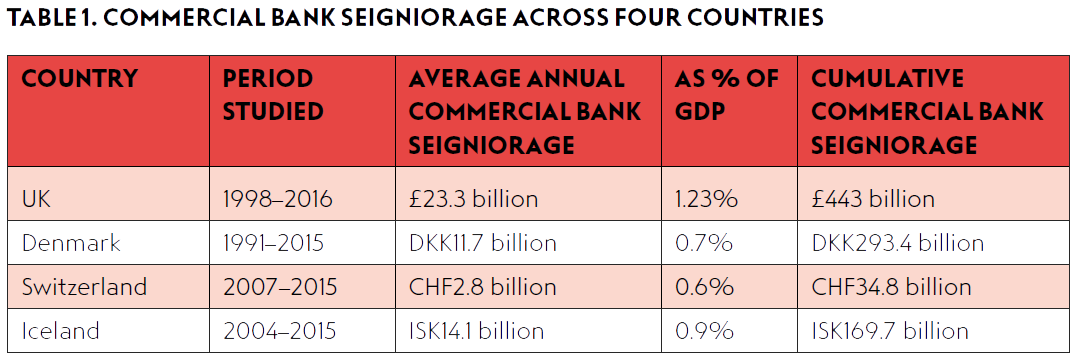

For the UK, we calculate that this privilege has provided commercial banks with seigniorage profits amounting to an annual average of £23 billion per year in the 1998 – 2016 period. This is equivalent to 1.23% of GDP. In contrast, state seigniorage – profits generated by central banks via the issuance of banknotes – has only amounted to £1.2 billion a year. We also examine commercial bank seigniorage in three other countries where there are active debates about monetary reform: Denmark, Switzerland, and Iceland (Table 1).

The findings suggest that a large proportion of banks’ profits are underpinned by their control over the money supply, an essential piece of public infrastructure. Should the public take back some control over the creation of money? A number of economists and civil society groups have argued that the central bank should create a higher proportion – or all – of the money supply. And a number of central banks, including the Bank of England and the Swedish central bank, are examining whether they should begin issuing central bank digital currency (CBDC). This would allow households and firms to directly hold digital money with central banks rather than with commercial banks.

Such a move could lead to a major increase in central bank seigniorage profits that would normally be reimbursed to the tax payer along with a corresponding decline in commercial bank seigniorage. For example, in the UK case, we find that £182 billion of cumulative seigniorage profits would have accrued to the public purse since 1998 if 30% of the money supply had been in the form of digital central bank currency rather than commercial bank deposits. This profit would have been paid to HM Treasury and could have been used to support public priorities or reduce the government deficit.

NFC smartphone contactless transaction

Commercial banks might argue that reductions in their seigniorage profits would lead them to contract their lending or charge higher interest rates. However, most bank lending in advanced economies flows in to commercial and domestic property and other financial assets rather than to businesses.

Seigniorage profits could be seen as another form of public subsidy for the banking sector, supporting excessive pay and non-value-creating lending that contributes to rising house price and financial-asset prices.

This means there is a strong case for returning a portion of seigniorage profits to the public purse by introducing CBDC. Such a move could also provide other advantages. It would create some genuine competition for the commercial banks in the payment services sector, levelling the playing field for non-bank financial intermediaries such as P2P lenders and the ‘Fin-tech’ sector and giving the public a genuinely safe way of holding its money. And it would give central banks a new channel to more directly stimulate the economy when necessary, for example via crediting households with ‘helicopter money’ or governments via ‘monetary financing’. Finally, it could help make the payments system and broader financial system more resilient to economic shocks.

Overall, such a reform would be a steptowards democratising a monetary system which – via seigniorage profits – gives commercial banks a major subsidy that puts them in a uniquely privileged position in the economy.

Topics Banking & finance