What next for the Euro?

The future of the single currency has huge implications for Britain - regardless of Brexit

02 January 2017

It is now 15 years since the introduction of the pinnacle of European Integration – the Euro.

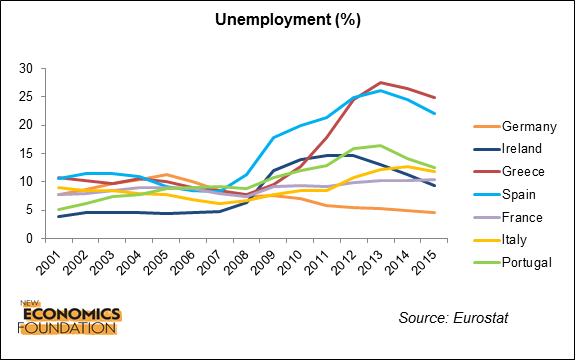

Yesterday’s anniversary comes at a moment of uncertainty for both the European Union (EU) and the Eurozone. The UK’s decision to leave the EU will see the first country exit since the signing of the Treaty of Rome. The Eurozone’s periphery is still in deep crisis, with unemployment rates ranging from 13% in Portugal to more than 20% in Spain and Greece. Populist, often nationalist, political movements are on the march across the continent.

The history of the Euro has been somewhat paradoxical: on the one hand, it was supposed to lead to further integration among the European people. On the other hand, it has divided the continent more than it has ever been since the end of World War Two.

Divisions exist both between and within countries. The division of Europe between “debtor” and “creditor” nations has provoked resentment between states, while increased inequalities and socio-economic insecurity across the continent has resulted in people feeling disempowered and disenchanted with the Europe ideal. Many people across the continent feel they have lost control over economic and policy outcomes which affect their everyday lives.

From the UK perspective, understanding what is happening in the Eurozone is of critical importance in the current political climate. If the problems in the Eurozone are misdiagnosed, false conclusions can be drawn and used to inform policy in the UK. At present, various misgivings about the Eurozone are being used by those making the case for a hard Brexit. In particular, it is often asserted that the problem with the EU and the Eurozone has been too much intervention by European institutions, leading for example to “overburdening regulation”.

However, these arguments are deeply misguided. As will be explored, many of the Eurozone’s problems can instead be traced back to a set of institutional arrangements which were based on the belief that self-regulating markets would lead to stability, prosperity and convergence (or poorer countries catching up with richer ones) — with little need for centralised economic management. As the UK moves ever closer towards a hard Brexit and a low tax, low regulation economy, the lessons from the Eurozone’s woes are more important than ever.

So what went wrong, and what should be done now? And does the euro have a future in these turbulent times?

The problematic architecture of the Euro

To understand what went wrong, it is important to first examine the basic premises behind the architecture of the Monetary Union – and their implications for Eurozone member States.

The basic idea behind the structure of the Euro was that self-regulating markets would ensure prosperity across the Eurozone as long as:

- Inflation was kept in check by the European Central Bank

- Member States had fiscal discipline, keeping their public deficits and public debt low

For these purposes, the European Central Bank was given a sole mandate to hit a 2% inflation target – regardless of patterns of unemployment and economic activity across the Eurozone. Unlike other Central Banks such as the US Federal Reserve, its mandate does not include ensuring price stability and guaranteeing full employment. Only the former is within the realm of its mandate.

Similarly, the Stability and Growth Pact required member states to ensure that their public deficit was kept below 3% of their national income (GDP) and their public debt did not exceed 60% of GDP.

When joining the EU, member States had already given up two levers of economic policy – trade policy and industrial policies (i.e. the protection of home grown industries). Joining the Euro meant member states were required to give up two other essential levers of economic policy – monetary policy and fiscal policy. In exchange for giving these up, they were promised that self-regulating markets would:

- Diffuse and decentralise productive capacity across the Eurozone, with each country specialising in what it does best to the benefit of all. The assumption here was that abolishing exchange rates would lower the last barrier to trade and increase specialisation among member-states. Increased specialisation would in turn translate into higher productivity and therefore higher living standards.

- Ensure that poorest countries of the monetary union would benefit the most. One aspect of this theory was that financial capital would flow from where it is abundant (richer countries) to where it is scarcer (poorer countries), lowering borrowing costs in the periphery of the Eurozone and consequently increasing private investment and growth rates. Eventually, all countries’ living standards would converge: Greece and Portugal would become as rich as Germany in a not-too-distant future.

The simplistic nature of these arrangements, and their risks, did not go unnoticed by observers of the time. Academic economists coming from very different backgrounds – including the American economist Milton Friedman, the British economist Wynne Godley and, long before them, fellow Brit Nicholas Kaldor – all saw fundamental flaws in the proposed design of the monetary union. At the time their critiques were dismissed, but with hindsight their insights have been proven correct.

Firstly, interest rates (set by Central Banks) and exchange rates are powerful adjustment mechanisms when a crisis hits. Before the Euro, when a country experienced a crisis resulting in unemployment and falling incomes, it could always respond by pursuing an expansionary monetary policy (by lowering its interest rates) and depreciating its currency to increase its exports and reduce its imports. Similarly, during a private sector slump, a country could always expand public sector spending to revive its economy. In a situation in which an unsustainable lending boom was underway, national Central Banks could always intervene to prevent the formation of financial bubbles (e.g. in the housing market). Without these mechanisms, countries experiencing a crisis would be condemned to harsh austerity and slashing wages to redress its imports and exports. In the now prophetic words of Wynne Godley,

“If a country or region has no power to devalue, and if it is not the beneficiary of a system of fiscal equalisation, then there is nothing to stop it suffering a process of cumulative and terminal decline leading, in the end, to emigration as the only alternative to poverty or starvation.”

Secondly, a centralised interest rate and exchange rate (for the entire Eurozone) set by the European Central Bank would not be a problem if all countries had a similar economic structure i.e. if their economic circumstances evolved in the same way. But if one country is booming while another is in recession, then a single monetary policy, based on average conditions across the monetary union, is problematic.

Before the launch of the Euro it was clear that member states were too different to be able to assume that they would experience the same economic cycles at the same time. In technical terms, the Euro was never an “optimal currency area” – and indeed even countries such as the UK and the US are not truly optimal currency areas. For example, London (which relies on financial services) and Aberdeen (which relies on oil and gas prices) may experience different economic cycles at different points in time. But in the UK and the US there are other mechanisms, outlined below, which act to even out these differences.

Thirdly, all the risks presented above can in theory be alleviated through centralised, federal institutions, and public intervention. But this required something more than simply leaving the market to determine economic outcomes. In the US, federal mechanisms and institutions redistribute wealth across the territory, to ensure minimum living standards in regions hit by crises or decline. Things like unified federal benefits, pensions or national insurance systems help smooth economic cycles across the US. Federal industrial policies can direct economic activity towards regions in decline. And people can easily emigrate from crisis-ridden regions to booming ones – more easily than they do in Europe. Finally, when a banking crisis hits, it is not regional states that are responsible for bailing out banks, but the Federal government.

“The woes of the Euro are not simply circumstantial, or just a product of the 2008 crisis”

None of these federal mechanisms exist in Europe. The critics of the common currency warned that when a crisis hit, neither national governments nor EU institutions would manage to do much to avert deep recessions and unemployment.

The woes of the Euro are therefore not simply circumstantial, or just a product of the 2008 crisis. The problem originated in the architecture of the common currency itself. People were led to believe that self-regulating markets would ensure a smooth functioning of the Eurozone. In fact, much more public action and control – albeit at a supranational level – were needed. Rather than creating a monetary union ahead of a federal political union, in hindsight it would have been more sensible to do things the other way around.

So what happened after the Euro was launched, and how did this compare with what was envisioned?

The good years (2001 — 2008)

The period between 2001 and 2008 is often referred to as the “success years” of the Euro: the period throughout which the common currency was delivering good economic outcomes for member States.

But even during this period the Eurozone’s economic growth was not particularly impressive, when compared to the US for example. It was also highly uneven; and more importantly, it masked vast imbalances which were building up within the Monetary Union.

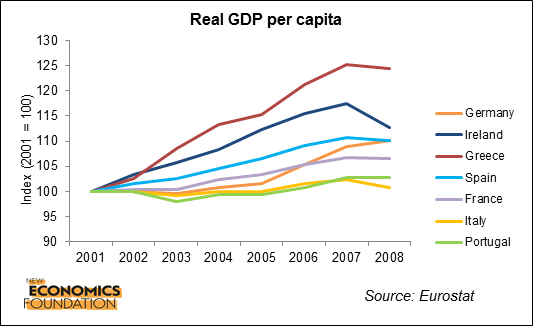

As the figure below shows, countries such as Italy and Portugal stagnated well before 2008. Before the crisis, the “success stories” of the Euro were Greece, Spain and Ireland. These countries were thought to provide a blueprint for convergence in living standards within the Eurozone: indeed they grew much faster than countries of the core, such as Germany, France or the Netherlands.

But beneath the surface, high growth rates were underpinned by unsustainable activities. Two of those proved the most critical: firstly, the financialisation of countries in the periphery, with unhindered cross-border capital flows creating unsustainable bubbles; secondly, the build-up of major trade imbalances between core and periphery countries.

Financial imbalances

Before the adoption of the Euro, cross-border capital flows were relatively constrained. When lending to a country like Greece, European banks would ask for high interest rates, which disincentivised cross-border borrowing. This is because the banks factored in exchange rate risks: constant devaluations and inflation were putting repayments at risk.

But when the Euro was launched, the landscape changed dramatically. The elimination of currency risks and the euphoria of financial markets dramatically reduced the interest rates at which peripheral states, banks and companies could borrow. Financial markets viewed it as safe to invest in Spanish banks and Greek government bonds as it was to invest in German banks and Dutch government bonds. From Athens to Madrid, a lending and borrowing spree was underway, with cheap public and private credit driving increased investment and growth.

Financial capital flowing from richer to poorer countries was exactly what theory predicted. So many viewed the spectacular increase in cross-border lending as good news: capital was flowing where it was scarcer, creating investment and growth where it was needed (in relatively poorer countries), and generating higher returns for the core’s financial institutions along the way. Self-regulating financial markets were good for all, delivering a triple whammy for the Eurozone.

However, in reality cross-border financial flows and low interest rates in the periphery were driving the creation of bubbles – for example in real estate markets – creating an illusion of wealth and prosperity in countries like Spain, Greece and Ireland. In Spain house prices doubled between 2001 and 2007. Cheap finance was not going towards productive activities, something which could have driven a genuine convergence with economies of the core. Rather, it made its returns by financing non-tradable activities such as real estate, construction and consumption. In some countries these bubbles were channelled through domestic banking systems (e.g. Ireland and Spain) and in others through public borrowing (e.g. Greece).

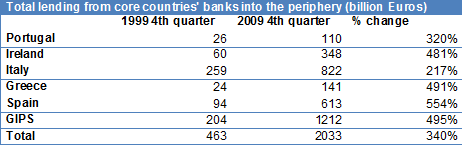

Member States and EU institutions did nothing to curb these bubbles. Locked-in a financial liberalisation mind-set where “markets know best”, they kept the system going while the financial sector lavishly kept financing the spree. By 2008, cross-border debts had grown massively. Bank assets as a percentage of GDP rose from 360% to 705% in Ireland, from 177% to 280% in Spain and from 148% to 220% in Italy. In Greece the budget deficit increased by 47% and private debt by 36% over the period.

Trade imbalances

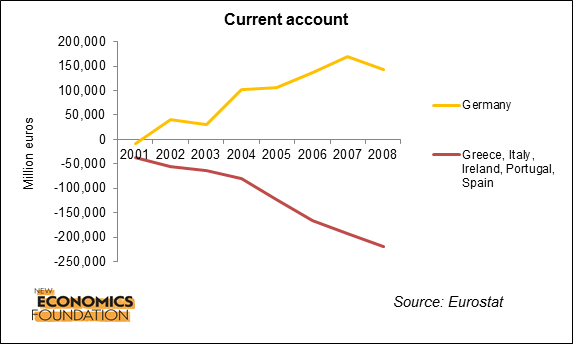

The pre-crisis years were also characterised by the build-up of sizeable trade imbalances. While countries of the core (e.g. Germany, the Netherlands, and Austria) were building up huge trade surpluses (exporting more than they imported) the opposite was happening in most countries of the periphery. In other words, poorer Eurozone countries were seeing their international competitiveness erode. Instead of leading to an equalisation of productive potential, the common currency was pushing towards the opposite: it was concentrating production in countries that were already highly competitive.

There are a number of reasons for this. Firstly, the huge capital flows towards the periphery, described earlier on, led to higher inflation in the periphery. This meant that their products became relatively more expensive – undermining their export base and making imports cheaper than national products.

Secondly, the Euro has historically been too strong relative to the economic characteristics of peripheral countries. A strong Euro probably hindered the exports of peripheral countries towards non-Eurozone members (e.g. the USA).

Finally, some academics have pointed to the economic policy pursued in the core countries, particularly labour market reforms and wage squeezes in Germany since the late 1990s, as contributing towards the Eurozone’s trade imbalances. Aside from increasing poverty and inequalities within Germany, these reforms constituted a “beggar-thy-neighbour” policy, which aimed at pushing German exports up and imports from other countries down.

“On the eve of 2008, the Eurozone was a currency area with major financial and trade imbalances”

In either case, trade imbalances and the direction of financial capital flows were closely entangled: countries posting a trade deficit needed to keep financing themselves by attracting cross-border lending if they were to maintain their living standards.

On the eve of 2008, the Eurozone was a currency area with major financial and trade imbalances. Instead of genuine convergence, the common currency area was already split between surplus (creditor) and deficit (debtor) nations. The entire European financial system, including banks of the core, was exposed to the financial bubbles of the periphery. The idea that self-regulated markets could truly deliver stability for the people and nations of the Eurozone was about to be seriously tested.

The global financial crash and the Eurozone crisis (2008 onwards)

After the collapse of Lehman Brothers in 2008, capital flows from the core to the periphery suddenly stopped as investors – mainly French and German banks – ceased lending across borders. Europe’s banking sector, which had invested heavily in US subprime mortgage backed securities, suffered large losses, and many states had to bail out several of their most affected banks. Across the Eurozone this resulted in debts shifting from the private sector to the public sector and budget deficits increased further as economic activity contracted, tax revenues fell and welfare spending increased.

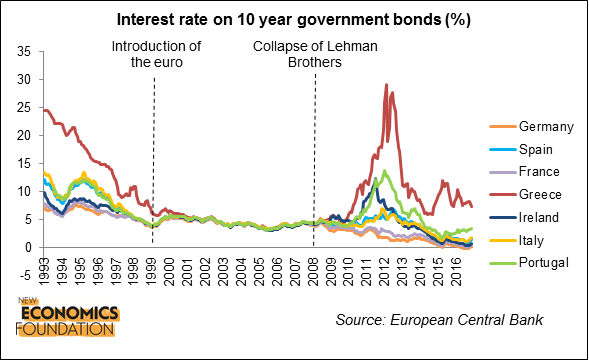

The abrupt halt to capital flows made it difficult for debt to be rolled over and raised concerns about the viability of banks and governments in the countries dependent on foreign lending, i.e. the periphery countries running current account deficits. Investors demanded higher returns for lending money, and interest rates on the sovereign bonds of periphery countries – which after the introduction of the euro had aligned with that of the core countries under the illusion of economic convergence – skyrocketed.

Periphery countries entered a vicious self-reinforcing cycle of rising borrowing costs and deteriorating budget deficits, as higher interest payments led to a worsening budget position, which in turn led to credit rating downgrades and higher borrowing costs, until eventually the position became unsustainable. Greece, as the Eurozone’s weakest economy, was the first to succumb to this feedback loop. By April 2010 it was apparent that Greece was becoming unable to raise sufficient finance on the markets and service its debts, and the Greek government was forced to request a bailout from the EU and International Monetary Fund (IMF).

As the crisis intensified, concerns spread to other small countries such as Ireland and Portugal, as well as to larger countries like Spain and Italy. In response, European policymakers established a number of mechanisms to provide financial assistance to Eurozone states in difficulty, including the European Financial Stability Facility (EFSF) and European Financial Stabilisation Mechanism (EFSM). The European Central Bank (ECB) – which thus far had done nothing to stem the unfolding crisis – eventually stepped in by providing cheap loans to European banks and intervening in sovereign bond markets. By the end of 2012 five Eurozone countries – Greece, Portugal, Ireland, Spain and Cyprus – had received emergency bailout packages.

The European institutions and the IMF were quick to blame the crisis on reckless behaviour from the periphery economies who, it was suggested, had lived beyond their means and became “uncompetitive” by allowing wages to increase too much. In contrast, countries such as Germany were held up as a model of competitive strength and fiscal prudence.

However, the empirical evidence supporting this explanation is weak. While Greece did increase public spending in the run up to the crisis, the governments of both Ireland and Spain – two of the supposedly fiscally reckless states – ran budget surpluses and kept within the limits for deficits and debts laid down by the stability and growth pact. In contrast, Germany was the first country to break the fiscal rules when it exceeded the deficit limits for four consecutive years beginning in 2003, and had a debt to GDP ratio far higher than that of Ireland and Spain when the crisis began. Belgium and Italy went into the crisis with debt to GDP ratios of around 100% of GDP and yet did not end up requiring bailouts. Studies have shown that there is no statistically significant correlation between pre-crisis increases in unit labour costs and economic performance.

Despite the global financial crash demonstrating serious flaws in the view that self-adjusting markets lead to stability and prosperity, European policymakers and the IMF insisted that the problem lay with the behaviour of individual countries, rather than recognise the flaws in the architecture of the euro.

The result was a hard line view that all debt must be repaid, even if it was clear that debt levels were unsustainably high. Governments were forced to implement severe cuts to public spending and increase taxes in order to reduce the fiscal deficit and public debt. Public assets were privatised, and labour markets were deregulated. Without having recourse to traditional macroeconomic policy tools to get the economy back on track, the only option for struggling economies was to attempt to boost competitiveness through reducing unit labour costs by drastically reducing wages – so called “internal devaluation”.

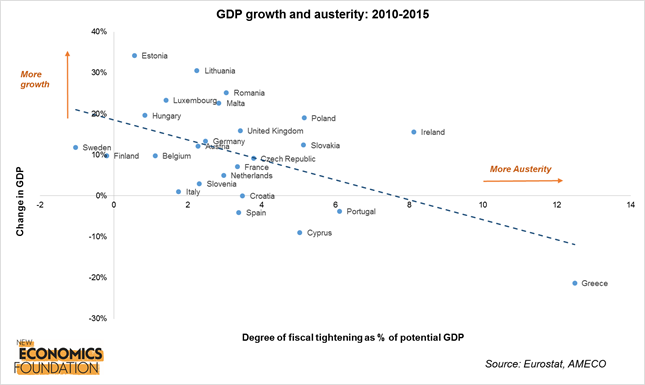

“Since the crisis, countries that have undergone the most severe austerity programmes have experienced the worst economic performance”

According to the EU institutions and the IMF, this programme of fiscal contraction and structural reform would lead to improved economic performance. However, the result was to push countries deeper into recession and undermine the productive capacities of the economy. In Greece, which has been subject to the most severe austerity measures, real GDP per capita has declined by more than 25%. Living standards have collapsed, and many Greeks have been left with little choice but to migrate. Across the periphery unemployment has ballooned, reaching over 25% in Spain and Greece. Youth unemployment peaked at 50%.

While cutting expenditure to pay off debt might make sense at a household level, pursuing this at the level of Government is counterproductive. When the Government cuts public spending, this reduces peoples’ incomes in the wider economy, and this in turn hurts tax revenues and undermines the economy’s productive capacity. Since the crisis, countries that have undergone the most severe austerity programmes have experienced the worst economic performance.

What next for the Euro?

The Eurozone enters 2017 facing its most challenging environment yet. With no resolution to its financial crisis in sight, and with numerous populist, often nationalist, political movements on the march across Europe, the next twelve months will be pivotal for the single currency.

Broadly speaking, there are three possible scenarios. The first is that there is a prolongation of the status quo, as political leaders fail to make fundamental reforms while also managing to stave off the threat from populist parties.

This would likely see the Eurozone economies continue to stagnate, as austerity measures sustain high unemployment and falling living standards in the periphery countries, while fiscal restraint in Germany and other core countries promotes conditions of weak demand across the Eurozone. The doubling down of existing imbalances would see the core and the periphery economies diverge even further, rendering the initial vision of Eurozone convergence a distant pipe dream.

Source: Eurostat

Given the suffering that has already been endured, the fragile social conditions in periphery countries and the emergent populist political climate, it is uncertain how long this scenario can be sustained for.

The second scenario is that the euro is dissolved and countries return to using their own national currencies. This could happen either by accident, for example if a major economy such as Italy voted to leave the euro, or through an organised dissolution by member states. Either way, a breakup of the Euro would be devastating, likely triggering what some academics have described as “the mother of all financial crises”. As soon member states switched to using new national currencies , most would experience rapid devaluation versus the old euro (with the exception of Germany and a few other core countries). Foreign holders of euro-denominated debt would suffer vast losses, and there would likely be defaults on a mass scale.

Since banks do not have to hold regulatory capital against sovereign bonds, the losses would force many European banks, which have invested heavily in the sovereign bonds of their parent states in recent years, into immediate bankruptcy. The financial shockwaves that would reverberate around the world would be immense, creating a crisis that would likely be many times more severe than the global financial crisis of 2008.

The UK, with its highly financialised and interconnected economy, would be caught up in a whirlwind of defaults, panics, bankruptcies and, most likely, state bailouts – regardless of whether it had opted for a hard or soft Brexit. As is always the case with economic crises, it would be those who can afford it least who would end up suffering the most.

“Reforms to make the Eurozone a properly functioning currency area for all its members… should be the overarching priority”

The third scenario is that European political leaders resolve to make sweeping reforms to the European architecture to make the Eurozone a properly functioning currency area for all its members. While undoubtedly posing major challenges, given the alternative options – economic catastrophe and a possible populist right wing insurgency – this should be the overarching priority of European policymakers.

So what needs to be done?

Firstly, there needs to be recognition that the current institutional arrangements are part of the problem, and that the underlying assumption that self-regulating markets will lead to stability, prosperity and convergence, is deeply flawed. If the Eurozone is to survive, then a degree of coordinated economic decision making is required.

As a minimum, this means introducing a system of Eurobonds, whereby Eurozone countries would raise finance as a coordinated bloc, rather than as individual states, with money subsequently being forwarded on to individual governments.

The effect of this would be to mutualise debt across the Eurozone, and avoid the situation whereby some states fall victim to global bond vigilantes, as happened in 2010. It also means creating a genuine banking union with common bank recovery and resolution mechanisms.

The mounting interdependence between domestic banks and their parent states that means that Eurozone crisis is as much a banking crisis as it is anything else. With the ongoing problem of non-performing loans plaguing Europe’s banks, it is essential that efforts are made to clean up Europe’s banking system, most likely with help from the ECB. This would also help reduce the capital flight underway in major countries such as Italy and Spain.

Perhaps most importantly, there is a need for a coordinated effort to stimulate demand in the Eurozone, for example by mobilising the European Investment Bank to direct investment to where it is most needed. Germany and other core countries should implement measures to boost national demand, for example by raising wages and boosting domestic consumption, to help create a bigger export market for peripheral economies.

Longer term, it is likely that a degree of federalisation is required, for example through a common unemployment benefit regime, to shield countries from asymmetric shocks and promote convergence.

“For European integration to succeed, the people of Europe need to be in the driving seat”

Second, and of equal importance, there needs to be a handing back of democratic control to the people of Europe. For European integration to succeed, the people of Europe need to be in the driving seat. This requires far more democratic EU institutions which are accountable to the aspirations of all people across the continent. This could involve increasing the prerogatives of the European Parliament, and placing both the ECB and the European Commission under more democratic control.

Given the bleak alternatives, it is reasonable to ask why none of this has happened already. Part of the reason for this lies in the fact that the Eurozone is made up of 19 nation states with long and proud histories, and issues of national interest, ideology and identity are always present. There are also legitimate questions of democracy – people are understandably reluctant to consent to sharing resources without appropriate democratic oversight.

However, with populist political movements on the move across Europe, the cost of inaction is high. Saving the economic prosperity of the Eurozone, and the political stability of Europe, depends on making a single currency work.

As the UK attempts to forge a new future outside the EU, learning from the Eurozone is more important than ever. More than anything else, the Eurozone crisis shows that relying on self-regulating markets to deliver stability and prosperity will deliver neither of those things.

Those calling for a hard Brexit should take note.

Topics Banking & finance Brexit