Exposed: the banks’ £23bn hidden subsidy

Who really controls our money? And how do we make it work for us?

31 January 2017

Who controls the creation of new money?

Many people might answer ‘the state’ or the ‘central bank’. But the hard currency printed by the Bank of England only amounts to 3% of the money in circulation in Britain today.

The rest? It’s created and allocated by commercial banks in the form of digital money – the pixelated numbers you see on your phone or computer screen.

Banks have close to complete control over the supply of new money, as we and others have long pointed out.

But today we and the Copenhagen Business School can reveal what this monopoly means in practice: an average annual banking bonus of £23bn. The likes of HSBC, RBS and Barclays are literally making money from money.

Where does this subsidy come from?

First, a historical term: ‘seigniorage’.

This refers to the profits that are generated through the creation of money. Traditionally this was the difference between the cost of physically producing currency and its purchasing power in the economy.

This money still exists, of course – the banknotes produced by our central banks. But it makes up just 3% of the money supply.

The other 97% is generated by banks as digital deposits in our bank accounts. Banks, unlike other lending platforms, do not have to acquire funds before making loans. Their IOUs have been privileged by the state as having the status of money.

You and I must hold bank liabilities in order to carry out everyday financial transactions – we have no choice (just trying paying your income tax without a bank account).

So today, ‘seigniorage’ is better explained as the difference between the interest rate that banks pay holders of their IOUs (deposits) and a benchmark market interest rate that non-bank issuers of debt pay on their IOUs. Banks pay less because their liabilities have the status of money. And they’re using this uneven playing field to generate huge annual profits.

Taking back control of Britain’s money

£23 billion a year — £443bn since 1998 — is a colossal sum, even as far as our banks are concerned. It represents 73% of banks’ profits after provision of taxes.

It’s yet another example of the generous public subsidies the banking sector enjoys, even as they fail to properly invest in our communities or small businesses.

The subsidy instead helps supports excessive pay and non-productive lending — only 10% of all bank lending in the UK supports businesses outside the financial sector.

With physical cash declining in proportion to electronic bank money, taxpayers have only a limited stake in this essential public infrastructure. Our research finds that, unlike the commercial banks, the Bank of England and HM Treasury makes just £1.3bn a year through their issuance of new bank notes.

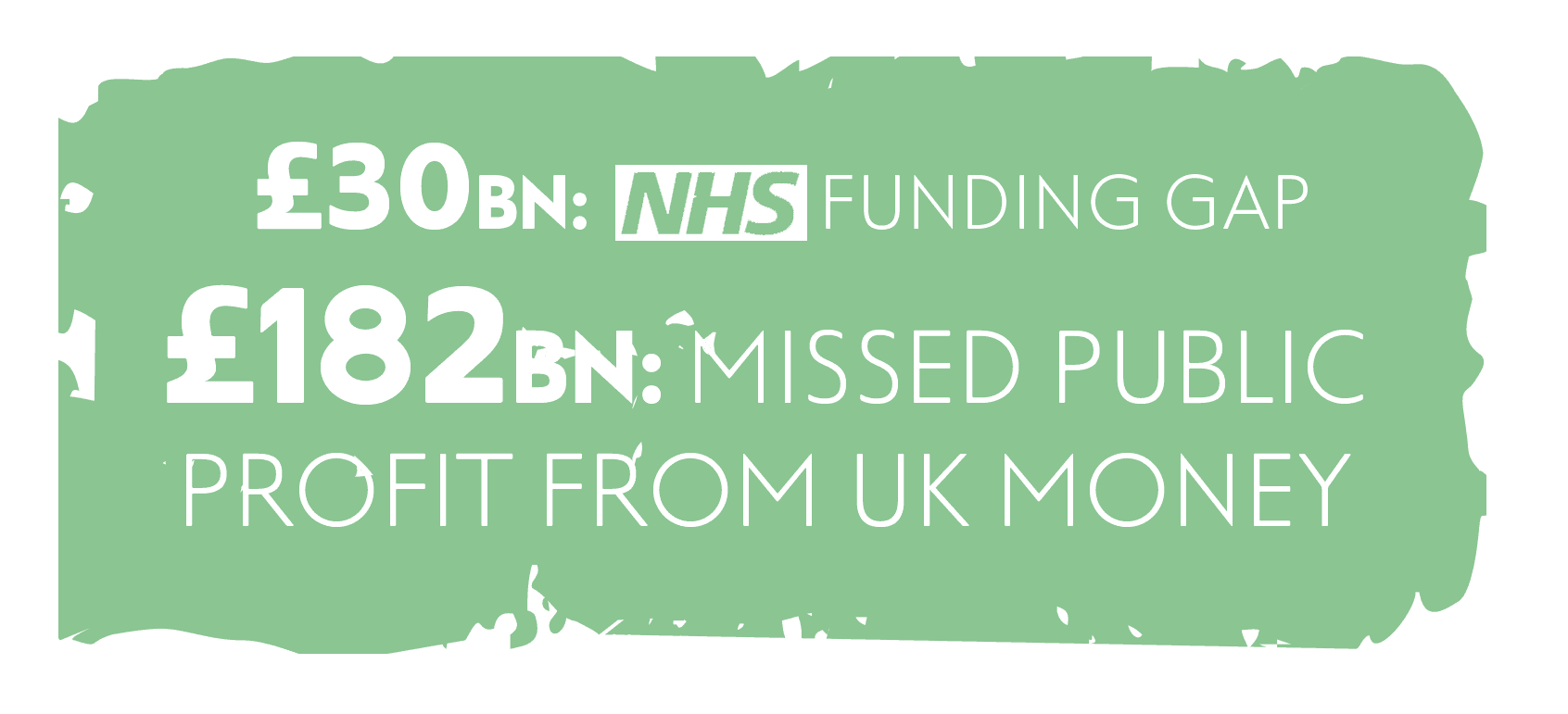

But if the Bank of England were to issue digital currency directly, the government could recapture seigniorage revenue for the public purse –just as it currently does with banknotes. We calculate that if just 30% of Britain’s money supply had been in the form of digital central bank currency instead of commercial bank deposits since 1998, the government would have gained £182bn — that’s over 6 times the projected NHS funding gap.

We’re not alone in thinking its time central banks considered digital money issuance. A number of other economists and civil society groups have argued that the central bank should create a higher proportion – or all – of the money supply. And central banks around the world, including the Bank of England and the Swedish central bank, are actively looking into it.

This would be a positive step, giving households and businesses a choice in whether to hold their money with commercial banks or with the central bank.

Central Bank Digital Currency could also provide other advantages. It would create some genuine competition for the commercial banks in the payment services sector, levelling the playing field for small competitors like P2P lenders and giving the public a genuinely safe way of holding its money. And it would give central banks a new channel to more directly stimulate the economy when necessary. What’s more, it could help make the broader financial system more resilient to economic shocks.

Commercial banks have a uniquely privileged position in our economy, but have consistently squandered the opportunities this represents. It’s time we took back control of our money supply.

Topics Banking & finance