This is what a real industrial strategy looks like

Why the government's current plans fall short

22 November 2016

Theresa May has pledged to deliver for working families, promising a more interventionist economic approach than her predecessor. In her CBI speech earlier this week she laid out some of the principles of what she calls “a modern industrial strategy”.

The Prime Minister has committed to increase research, development and support for innovation by £2bn over the course of this parliament, and enhance infrastructure investment, committing £1bn for faster broadband across the UK.

She also announced the launch of an inquiry on “patient capital” — how to improve funding support for SMEs – and the use of strategic public sector procurement.

Bar the backtracking on putting workers’ on company boards, these steps are in the right direction. But they are timid and narrow — falling short of the urgent challenges facing the UK’s dysfunctional and unbalanced economy.

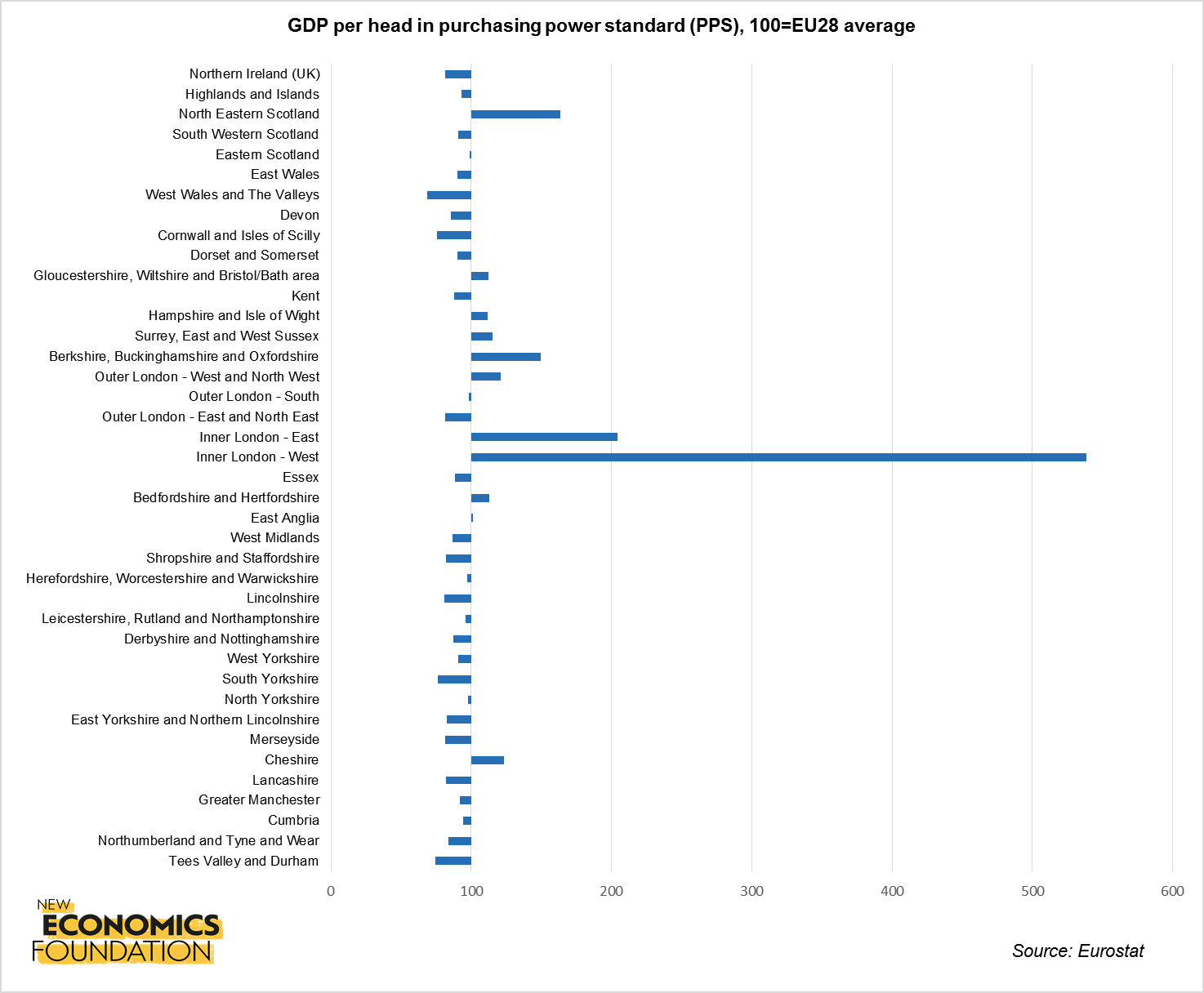

The scale of the problem is huge: out of the 40 NUTS‑2 regions of the UK, 29 have an income per head which is below EU28 average – an average which includes the poorest countries of the EU.

It’s the devastating legacy of an economy that has consistently put the interests of the City of London ahead of the rest of the country. An industrial policy aiming to rebalance the UK economy must be bigger, bolder and driven by the regions who need it most.

Five principles for a modern industrial strategy

1. Give regions and local people the control they need to transform their futures

Local and regional bodies need autonomy to formulate and implement development plans which are consistent with their region’s advantages and the aspirations of local people.

A command-and-control approach, where development plans are mandated by central government, will fail to rebalance the economy – as it has done for more than three decades.

Decentralising decision-making should walk hand-in-hand with more decentralised financial capabilities – including local banks, a bigger budget for local and regional authorities, and a network of development banks.

2. Invest now for a more productive, prosperous economy

The government must commit the funds needed for national and regional development.

For example, Theresa May’s £2bn pledge for additional research and development support is not enough to close persistent gap between the UK and other advanced economies. The government’s unwillingness to invest more in our shared future is one of the causes of the UK’s appalling productivity performance.

3. Properly value our core economy

To deliver an effective industrial strategy we need to invest in the UK’s most vital asset – the individuals, families, people and places that make up its core economy.

That will require a huge effort to close the educational gap, investment in health and social infrastructure around the country, and supporting sectors of the economy which can deliver good jobs – not merely productivity growth. A healthy economy depends on a healthy society.

4. Ensure sustainability for future generations

Good industrial policy means compatibility with our transition to a low carbon economy. Our reluctance to “pick winners” or “pick sectors” is counterproductive – a green industrial strategy requires investment in thesectors that will future-proof our economy. As our Action Plan for the UK coast shows, investing in decentralised renewable energy and energy efficiency would create hundreds of thousands of new jobs across the country.

5. Give employees control of their working lives

We all deserve a stake in the new technologies and industries that are reshaping our economy. A modern industrial strategy needs to give workers real control over their working lives – spreading decision-making within companies, ensuring minimum labour standards, strengthening workers and union representation, and increasing wages.

The government rightly thinks that the state should do more to rebalance the economy. We now need to mobilise our shared resources to build a new economy based on the experience, expertise and potential of people across the UK.

Photo credit: Olga Kofanova

Topics Macroeconomics Work & pay