To achieve real change, the UK must rewire it’s financial system

Reflections from our joint event with Triodos Bank on the need to overhaul the financial system

17 June 2026

Soaring inequality, failing public services, environmental breakdown, the suffering of former industrial areas – the UK needs fundamental change which this government has so far failed to deliver. But there’s a missing piece of the puzzle when politicians and the media talk about why the UK economy is failing to achieve better outcomes. None of the problems we face can be explained without facing up to fundamental issues with the financial system.

Put simply, the current financial system rewards investors for channelling finance into harmful, speculative, or destabilising activities, while failing to deliver enough finance for investing in the things our society actually needs. Any government that wants to tackle falling living standards, boost regional economies, and protect us from the fallout of climate breakdown will need to tackle the incentives baked into the financial system itself.

To build upon our shared desire to see change in the financial system, we recently hosted an event with Triodos Bank, the sustainable bank who are campaigning for a different way of doing finance. Triodos recently released a report calling for a fundamental overhaul of the financial system, including the introduction of a publicly-owned payments system and a democratic framework to guide finance away from harmful activities and towards socially and environmentally beneficial uses. At NEF we have been calling for credit guidance in the form of an Economic Coordination Council, which would also enable better management of inflation and healthier government finances.

In his opening speech, Triodos’ chief economist Hans Stegeman argued that the financial sector is too big and has incentives that are fundamentally misaligned with the rest of society. Since financial actors are only incentivised to chase the highest possible financial returns, and don’t bare the costs of the risks and harms they create, if left to itself, the finance sector will continue to drive us down a destructive path.

To build upon our shared desire to see change in the financial system, we recently hosted an event with Triodos Bank, the sustainable bank who are campaigning for a different way of doing finance. Triodos recently released a report calling for a fundamental overhaul of the financial system, including the introduction of a publicly-owned payments system and a democratic framework to guide finance away from harmful activities and towards socially and environmentally beneficial uses. At NEF we have been calling for credit guidance in the form of an Economic Coordination Council, which would also enable better management of inflation and healthier government finances.

In his opening speech, Triodos’ chief economist Hans Stegeman argued that the financial sector is too big and has incentives that are fundamentally misaligned with the rest of society. Since financial actors are only incentivised to chase the highest possible financial returns, and don’t bare the costs of the risks and harms they create, if left to itself, the finance sector will continue to drive us down a destructive path.

In the expert panel that followed, Jesse Griffiths – CEO of Finance Innovation Lab – agreed with Hans’ characterisation of the financial sector. He argued that growing the UK’s financial sector should not be a policy goal in itself as a larger finance sector does not necessarily equate to a more successful economy. In fact, economic research shows that for developed countries, a larger financial sector actually damages economic activity. Instead of growing the financial sector, the goal should instead be to increase the amount of financing that goes to productive investments in the real physical economy, while decreasing harmful and risky forms of finance. Jesse also called for the government to play a more proactive role in infrastructure investment by expanding public finance institutions such as the National Wealth Fund.

Ann Pettifor, the renowned macroeconomist who successfully predicted the 2008 financial crisis, agreed with the need for a fundamental overhaul of the financial system, but placed a particular emphasis on the need for introducing democratic controls over how investors are allowed to move money between countries. The untethered movement of international finance means that countries are much less able to control their interest rates at home, which is crucial if we expect individuals, businesses and governments to invest in the green transition.

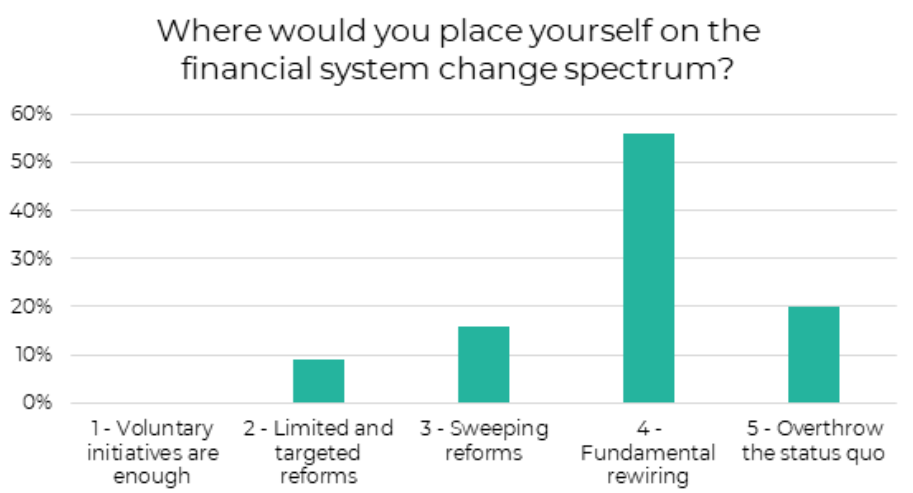

Finally, we heard a note of caution came from James Alexander, the chief executive of the UK Sustainable Investment and Finance Association. He challenged whether the problem is mainly with the financial system itself, or with the incentives and regulations of the real physical economy: If the incentives are right, then the finance will flow. For example, if investors could be confident that governments would stick to a clear and stable timeline for the phaseout of petrol cars, then investing in electric vehicles would make more sense. Rather than blaming the financial system, why don’t we just ban the things we don’t want and subsidise the things we do want? However, as the poll below shows, the majority of the audience clearly thought that the financial system itself needs radical change too.

As the UK tries to work out a new economic direction, there are two key takeaways that stand out to me from this event. Firstly, growing the financial sector should not be an end in itself, and could even make things worse. Instead, the focus should be on reshaping the financial system to drive positive outcomes elsewhere in the economy. Secondly, achieving real change will require real disruption. Fundamental rewiring will be impossible without some level of confrontation with the entrenched financial interests who benefit from the status quo. Whoever wants to change Britain for the better needs to be up for a fight.